Derivatives trading in India has matured considerably over the past decade, and with that maturity has come a deeper appreciation among active traders for the analytical tools available beyond basic charting. Among these, the data embedded in the Nifty Option Chain has become a cornerstone of how informed market participants assess the likely direction and range of index movement each week. For those who trade the banking index exclusively, the Bank Nifty Option Chain carries the same analytical weight but with the added dimension of higher volatility and more frequent intraday swings. Taken together, these two data sources offer a window into market psychology that is difficult to replicate through any other analytical method.

Understanding the Architecture of Option Chain Data

The option chain presents data in a structured format that, at first glance, can appear overwhelming. Columns for last traded price, bid-ask spread, implied volatility, change in OI, volume, and open interest line up across dozens of strike prices. The challenge for a new trader is knowing which of these columns deserves the most attention and in what sequence.

The most seasoned traders typically begin with open interest. They identify the strikes with the highest absolute OI on both the call and put side, as these establish the immediate reference range for the index. The next layer of analysis involves looking at changes in OI from the previous session. A strike that has seen a sudden and sharp build-up in fresh OI overnight is likely responding to some new information or conviction in the market. This is worth investigating further before the trading session begins.

After identifying the key OI levels, traders move to implied volatility. If IV is elevated compared to recent averages, it suggests the market is nervous. If IV is unusually low, it often points to complacency, which can itself be a contrarian signal. The interplay between these data points paints a nuanced picture that no single column can provide on its own.

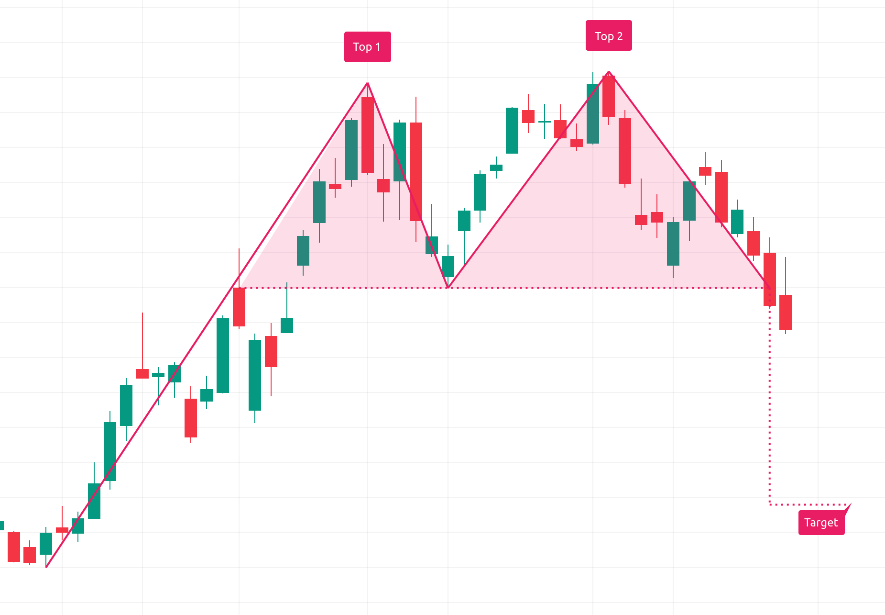

The Concept of Pain and Anchoring in Weekly Expiry

In the context of weekly options, the concept of max pain plays a surprisingly important role in how prices behave near expiry. Max pain is the price level at which the total value of all outstanding option contracts is minimised, meaning the maximum number of contracts expire with zero or minimal value for their holders.

While it is tempting to treat max pain as a precise prediction, a more accurate interpretation is to use it as a reference zone. Prices tend to be pulled toward this level, not because of any single large player manipulating the market, but because the collective hedging activity of many option writers creates buying and selling pressure that converges around the max pain point.

Traders who observe this phenomenon over multiple expiry cycles begin to develop an intuitive feel for how prices behave in the final two hours before expiry. Knowing the max pain level going into the final session of the week gives you a baseline expectation against which to measure actual price behaviour.

Using PCR Extremes as Contrarian Signals

The put-call ratio is among the most straightforward sentiment tools derived from option chain data. At its simplest, it tells you how many put contracts are open relative to call contracts. But its real analytical value emerges at the extremes rather than at neutral readings.

When PCR rises sharply and reaches levels not seen in recent weeks, it typically reflects a market that has become excessively fearful. A large number of traders have purchased puts as protection or as directional bets against a further decline. This kind of positioning creates a crowded trade, and crowded trades have a habit of unwinding painfully for those caught on the wrong side.

Historically, very high PCR readings in the Indian market have often preceded short-term reversals to the upside, not because the fundamentals changed but because the excessive pessimism itself became the trigger for a squeeze. Short sellers and put buyers closing their positions creates buying pressure that lifts the market even in the absence of positive news.

The reverse also holds. A very low PCR reflects too much optimism. Traders are not buying puts because they feel confident about the upside. This complacency can reverse quickly when any unexpected negative catalyst emerges, catching the majority of participants off guard.

Time Decay as a Strategic Tool

Theta, or time decay, is the erosion of option premium with the passage of time. For option buyers, theta is a constant enemy. Every day that passes without a significant move reduces the value of their position, regardless of whether the underlying price stays flat, moves slightly in their favour, or moves slightly against them.

For option sellers, theta is an ally. Writing options and collecting premiums while time erodes their value is the foundation of many of the most consistently profitable derivatives strategies. The challenge is managing the tail risk that comes with option writing, which requires either position sizing discipline, hedging through spreads, or active monitoring with predefined stop levels.

The option chain helps sellers identify which strikes offer the best balance between premium received and distance from the current market price. Strikes that are far out of the money offer safety but a minimal premium. Strikes close to the current price offer attractive premiums but carry far greater risk if the market moves decisively in one direction.

Developing Judgment Through Consistent Observation

Often, no amount of theoretical understanding of alternative chain valuation can replace the judgment that comes from continually looking at how the facts behave in real market conditions. Traders who observe the series daily, follow their observations, and musical results in more than one completion cycle, detail a form of the market trend that makes their knowledge of the curve particularly rapid.

The easiest way to build this awareness is to keep a grounded journal. Every morning before the market opens, record the OI level, create a PCR word, note the maximum pain level, and write down estimates of trading variation if possible for the day. At the end of the session, review what happened to your expectations. Over the course of weeks and months, patterns emerge that refine your framework and make your analysis progressively sharper and more reliable.